2 hours ago

2 hours ago

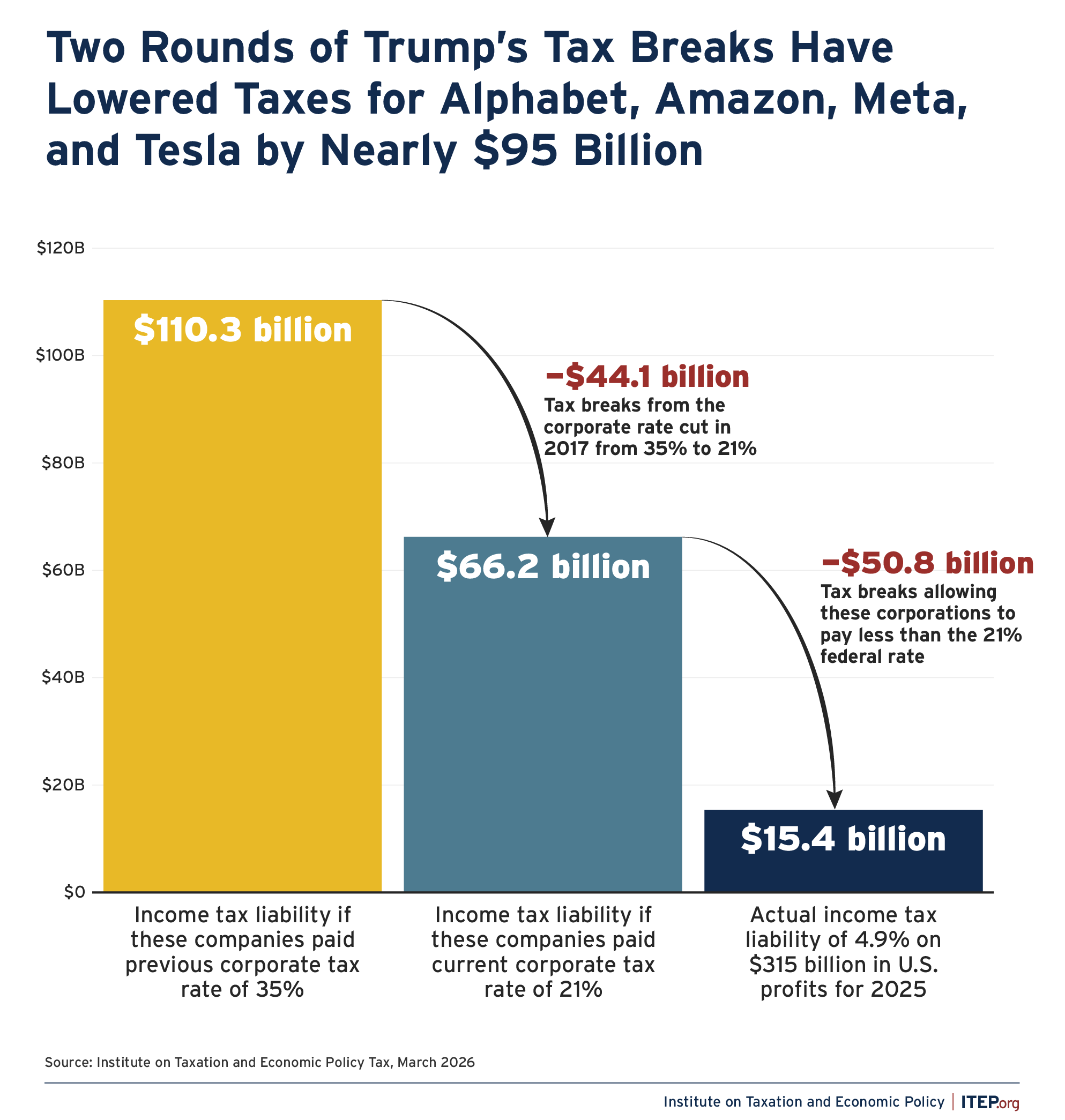

In February, ITEP reported that four huge tech companies with pro-Trump CEOs paid just 4.9 percent of their profits in federal corporate taxes in 2025 (and saved $51 billion compared to what they would pay at the full 21 percent tax rate). That prompts the question: How did these companies do it?

Part of the answer: the leaders of these companies publicly supported Trump to ensure the most favorable policies possible. Their CEOs, Mark Zuckerberg (Meta, owner of Facebook), Jeff Bezos (Amazon), Sundar Pichai (Alphabet, owner of Google), and Elon Musk (Tesla), attended Trump’s 2025 inauguration. And Trump delivered for them, both in his 2017 tax bill and again in 2025 with the so-called “One Big Beautiful Bill Act” (OBBBA).

More specifically, the four companies used a collection of tax breaks, some of which pre-dated Trump’s presidency and others that were created in the 2017 law or OBBBA.

These tax breaks collectively saved the companies nearly $51 billion in 2025 compared to what they would have paid if their federal income tax bill equaled 21 percent of their profits, instead of just 4.9 percent of their profits.

But President Trump has saved them even more. The statutory federal corporate income tax rate was 35 percent before his 2017 tax law slashed it to 21 percent. If these companies had paid 35 percent of their profits in federal income taxes, they would have collectively paid another $44 billion in taxes, as illustrated below.

Figure 1

Download Figure 1

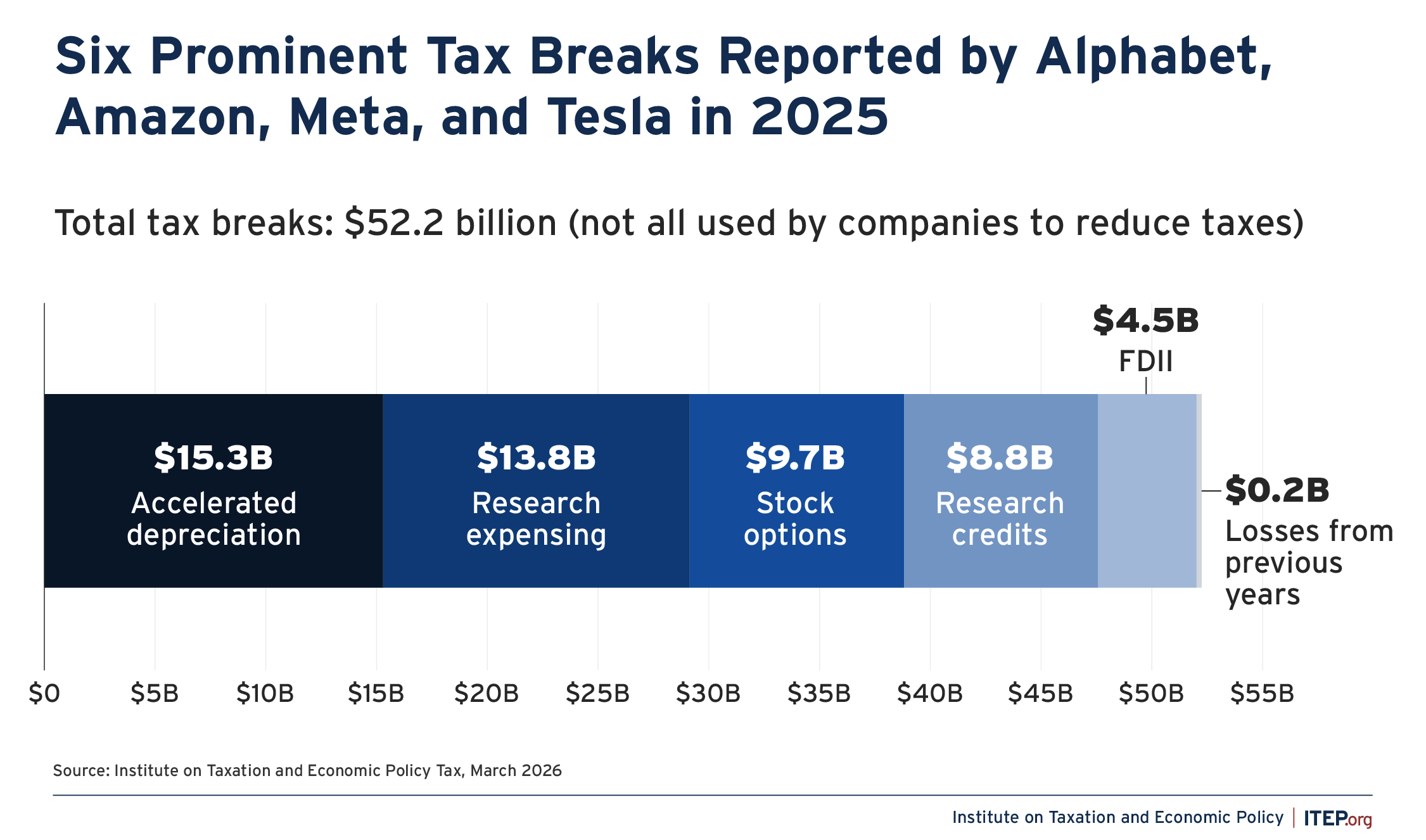

The tax breaks allowing the companies to pay less than the statutory corporate tax rate of 21 percent fall into several different categories. Corporations are not entirely consistent in disclosing these details, but Figure 2 below illustrates what the four tech companies collectively report about the most common tax breaks.

Figure 2

Download Figure 2

More Details About Types of Tax Breaks Used by the Four Tech Companies

Research Expensing

When a company spends money on research, it is essentially making an investment to create an asset in the form of knowledge or innovation that did not previously exist. In at least some situations, the companies should arguably be required to write off investments in research over several years, the way they write off other investments. But research is treated as an expense under financial accounting rules and tax rules.

The 2017 tax law, while generally favoring high-income people and corporations, removed this generous tax treatment of research and instead required all companies to amortize research spending over five years. Drafters presented the five-year amortization for research as a way to raise revenue that would partly offset the cost of the tax cuts in the law, but its authors likely never intended for this tax increase to remain in statute. And in fact, the 2025 tax law (OBBBA) reinstates research expensing permanently.

Some activities subsidized by this tax break do not meet any definition of “research” that most people would understand. Companies urging Congress to extend this tax break ranged from a brewery and a company that develops frozen and packaged foods to a sausage business and a company that develops electronic games for casinos. Lawmakers should have asked what “research” this tax break supports before blindly reinstating it.

The astonishing part is that OBBBA effectively allows companies to retroactively take deductions for research expensing for the years they were barred from doing so by the 2017 law. (OBBBA provides research breaks that are literally retroactive for smaller companies and effectively retroactive for larger companies in most situations.) The research expensing provision is supposedly an incentive for businesses to conduct research that could benefit society, but rewarding companies for what they did in the past with a retroactive tax break is obviously not such an incentive.

The four tech companies collectively reported $13.8 billion in savings from this effectively retroactive research expensing in 2025.

Accelerated Depreciation

Provisions for accelerated depreciation allow companies to write off the costs of investments in equipment more quickly than the equipment wears out and loses value. The most likely outcome is that this rewards companies for making investments they would have made absent any tax break. The 2017 Trump tax law allowed companies to immediately write off the full cost of investments, which is the most extreme version of accelerated depreciation. This “bonus depreciation” was scheduled to eventually phase out under the 2017 law, but OBBBA reinstated it permanently.

In theory, accelerated depreciation is merely a shift in the timing of tax payments. Tax deductions that would otherwise be taken later are taken now, and taxes that would otherwise be paid now are paid later. But companies that continue to take advantage of accelerated depreciation can make this benefit last a very long time or indefinitely and essentially enjoy interest-free loans from the IRS.

The four tech companies collectively reported $15.3 billion in tax savings from accelerated depreciation.

Stock Options

Some companies reduce their taxes by using a break for stock options that they typically pay to their executives. This tax break allows companies to write off stock-option-related expenses for tax purposes that go far beyond expenses they report to investors.

The benefit of this tax break tends to go overwhelmingly to a small number of highly profitable companies in the tech sector.

The four tech companies collectively reported $9.7 billion in tax savings from stock options in 2025.

Research Credit

Companies sometimes receive a tax credit for activities they characterize as research. This research tax credit is even more beneficial to them than the research expensing provision, which is generally used for activities that do not qualify for the research credit.

As with research expensing, lawmakers seem to have paid almost no attention to the question of what activities are being subsidized with this tax break and whether any normal person would call them “research” or think they are worthy of a tax break.

For example, Intuit, which lobbied Congress and the administration to shut down the IRS’s new, free online tax filing so that taxpayers would feel forced to use its TurboTax software, has claimed research tax credits that may exceed the entire cost of that free online tax filing program.

In other words, taxpayers are providing a subsidy through the tax code for Intuit to do “research” that may involve further developing the tax filing software that people are now forced to use thanks to the corporation’s lobbying.

The four tech companies collectively report $8.8 billion of research credits in 2025.

Foreign-Derived Intangible Income (FDII)

The FDII deduction was enacted as part of the 2017 Trump tax law and later expanded and renamed under OBBBA. This provision provided a special, lower effective tax rate on income earned from intangible assets, such as patents, trademarks, and other forms of intellectual property, by selling products abroad. As ITEP has previously noted, FDII benefits have gone disproportionately to very large corporations in industries that are heavily reliant on intangible assets, like tech and pharmaceuticals, thereby creating a tax code that treats different sectors of the economy much differently. These are also precisely the economic sectors whose leaders have been consistently found to have artificially shifted their U.S. income into tax havens for the past quarter-century.

The four tech companies collectively report more than $4.5 billion of FDDEI benefits in 2025.

Losses from Previous Years

Even if a company was profitable in 2025 (as were the four tech corporations in this report) they could nonetheless apply losses from previous years to reduce the profits subject to income tax.

When corporations have deductions that reduce their taxable income, they generally cannot use those deductions to reduce income below zero. Instead, they are allowed to carry forward the resulting losses to a future year when they do have positive taxable income to offset.

The four tech companies collectively paid $0.2 billion ($200 million) less in federal income taxes in 2025 because of net operating losses from previous years.

What About the Minimum Tax That Is Supposed to Apply to Big Corporations?

A provision often called the Corporate Alternative Minimum Tax (CAMT), enacted as part of President Biden’s Inflation Reduction Act, prevents certain types of tax avoidance but does not seem to have had an impact on these four tech companies in 2025.

The CAMT applies to the biggest corporations, those reporting profits averaging more than $1 billion a year for three years. It is calculated (with several complicated exceptions) as 15 percent of the profits that these corporations report to their shareholders, which can be greater than the profits they report to the IRS under the regular tax rules.

The idea behind the CAMT is that no matter how many tax breaks Congress provides to corporations, large corporations should pay a minimal amount of taxes if they are reporting profits to their investors under financial accounting rules.

The problem is that lawmakers weakened the CAMT with exceptions to preserve certain tax breaks, particularly expensing and other types of accelerated depreciation used by the four tech companies.

The CAMT is nonetheless likely to serve an important purpose and block some of the most egregious corporate tax avoidance and may have a significant impact on these tech companies in the future. Meta recently reported that the CAMT will reduce the amount of tax savings it would otherwise receive from OBBBA by about $16 billion.

Another problem is that the Trump administration has further weakened the CAMT with regulations that clearly violate the statute they supposedly implement. For example, the Treasury Department recently proposed a regulation pretending that the CAMT was written to exempt the retroactive research expensing allowed under OBBBA. This may allow Meta to access most of the $16 billion in tax savings that the company complained it would otherwise be denied.